Reach out to our friendly team at Atlas Broker who will be able to guide you in the right direction.

Where are rates going?

This is one of the most common questions a broker is asked by clients, whether it be existing or new referrals. A broker has two options here:

- You rant on the pros/cons of an increase/decrease, rattle off some macroeconomic data, sprinkle it with anecdotal insights from businesses you work with & add a witty quip about the incoming governor being a dove/hawk…

or - You hit them with God’s honest, yet oh so unfulfilling answer ‘your guess is as good as mine’.

Why do the rates change at all? At its most basic level, the reserve bank (RBA) adjusts the cash rate to either stimulate the economy (as done through 2020) or suppress economic activity (as we are seeing now). The higher the rates, the more a saver earns on cash in the bank & the less cash borrowers have to spend. This has the effect of decreasing spending on goods & services, thus cooling their prices.

The RBA has a dual mandate, it’s two responsibilities are to maintain:

- full employment (everybody than can & will work gets a job)

- price stability (goods/services prices steadily grow year in year out)

A trip to your grocery store or a quote from a local tradie is all the evidence you need that prices are not stable (although employment is very strong). It’s confusing to hear that the RBA wants to ‘crack the job market’, increasing unemployment to decrease pressure on wages so people reign in spending. It’s like robbing Peter to pay Paul.

Odds are you have had the rates conversation around the BBQ or on the sidelines of your child’s sporting games. There is always someone who seems to me be ‘in the know’, speaking with the authority & confidence of a pro!

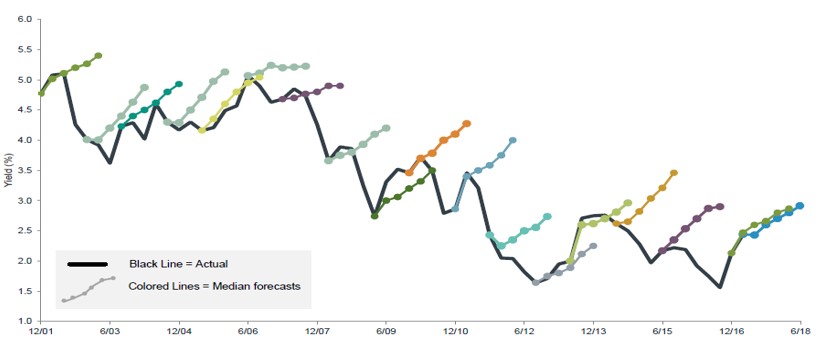

This begs the question, how accurate are rate predictions in general? The chart below shows the actual rate (black line) vs expert predictions (coloured lines). As you can see, the expert predictions are far from accurate, but that doesn’t stop a punter from having a crack, despite the odds. After all, you gotta be in it to win it!

So what do I think? For conversations sake, hiking is likely maxed out for this cycle or one more & done at most. Why? increases work with long and variable lags, as it takes time for lenders to pass them on, for household savings to be eroded & the business/consumers to fully feel the effect on their cashflows. The new governor will likely give it some time to see the true effects of the sharpest tightening cycle in decades, as this would be the prudent thing to do.

And on that note, I leave you with a quote I wholeheartedly agree with:

“There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know,” John Kenneth Galbraith.

– Sam McDonald

Reach out to our friendly team at Atlas Broker who will be able to guide you in the right direction.